[ad_1]

Amassing a standard safety deposit has at all times simply been part of the leasing course of. However at the moment, that upfront value will be out of attain for a lot of renters.

Featured Provide

Begin your free trial at the moment!

Attempt Buildium free of charge for 14 days. No bank card wanted.

Begin Your Trial

To get extra residents by way of the door, some property managers supply safety deposit alternate options. Right here’s how these applications work, and why they is perhaps a wise transfer for your corporation.

What Are Safety Deposit Options?

Safety deposit alternate options are monetary applications that substitute the normal lump-sum deposit with a extra versatile possibility—often smaller month-to-month funds unfold out over the lease time period.

They’re designed to ease the monetary burden on renters whereas nonetheless providing safety for property managers in case of harm or missed hire. And in lots of circumstances, they arrive with added perks for either side.

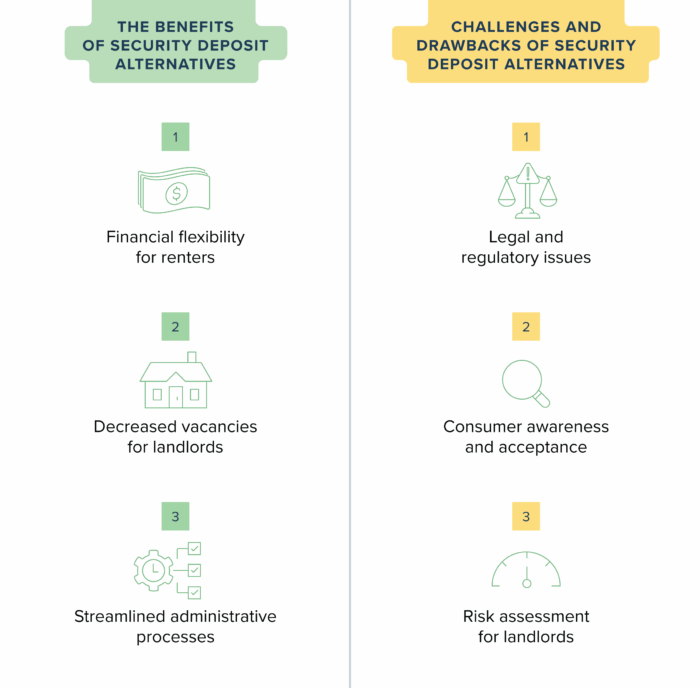

The Advantages of Safety Deposit Options

There are lots of advantages to going with safety deposit alternate options, together with:

- Monetary flexibility for renters: Some renters will recognize being able to finances round a smaller, recurring fee moderately than making a prohibitively-large one upfront. Others will like the thought of having the ability to let extra of their cash earn curiosity in their very own accounts moderately than another person’s escrow account.

- Decreased vacancies for landlords: Providing versatile choices can open the door to extra certified candidates, particularly those that is perhaps held again by a big upfront deposit. With a wider pool of renters, you’re extra more likely to fill models sooner and preserve emptiness charges low.

- Streamlined administrative processes: Since third-party suppliers usually deal with these applications, property managers can skip the trouble of gathering, holding, and refunding deposits—and deal with different components of the enterprise.

Challenges and Drawbacks of Safety Deposit Options

Nonetheless, like all monetary choice, providing safety deposit alternate options can even include a couple of drawbacks, together with:

- Authorized and regulatory points: Safety deposit alternate options are comparatively new. It’s necessary to verify any various program you select complies together with your state and native rules. Some areas might restrict use. You’ll additionally seemingly should have a separate settlement on file outlining your relationship with the third-party supplier, in addition to the tenants.

- Shopper consciousness and acceptance: Since these preparations are newer, renters is probably not as conscious of them and hesitant to simply accept them as a viable various to a standard safety deposit.

- Danger evaluation for landlords: There’s nonetheless some inherent threat with these applications. For instance, an insurance coverage coverage might discover a cause to disclaim the declare if there’s harm to the unit. Make sure you learn the phrases and situations of any various program you’re contemplating very rigorously and to elucidate the potential dangers to your landlords.

Varieties of Safety Deposit Options

So, what are the several types of various applications accessible to you? Beneath are 5 choices to think about using in your property administration enterprise.

1. Surety Bonds

A surety bond works equally to a bail bond. On this case, the tenant pays an upfront deposit on the bond, usually 17.5% to twenty% of its worth. Then, if there’s harm to the property on the finish of the lease time period, you place a declare with the surety bond firm, who will then compensate you for the work and search reimbursement out of your former tenant.

Professionals

- Immediate fee: Many surety bond corporations pays out shortly for claims, permitting you to show over the property sooner.

- Further screening: Most surety bond corporations will full their very own further tenant screening processes earlier than agreeing to challenge the bond.

- Much less administrative burden: On this case, the surety bond firm handles the gathering course of and, often, any litigation that arises on account of disputes.

Cons

- Restricted protection: As with all insurance coverage coverage, surety bonds have a scope of protection that’s restricted by the phrases of their agreements. In case your declare falls exterior that scope, it is probably not coated.

- Decrease incentive for tenants: Residents gained’t get their bond deposit again on the finish of the lease, probably giving them much less incentive to take excellent care of the property throughout the lease time period.

- Larger prices after claims: If you happen to make a declare towards a surety bond, securing future bonds might come at the next value or approval could also be harder.

When to make use of surety bonds

Surety bonds are sometimes seen in high-cost areas, the place making a full safety deposit could be value prohibitive for almost all of renters. They’re additionally utilized in conditions the place potential residents might have fewer monetary assets, comparable to scholar housing preparations.

2. Third-Occasion Safety Deposit Different Providers

Some third-party platforms focus particularly on safety deposit alternate options. Whereas their fashions might differ, the objective is identical: scale back upfront prices for renters whereas defending the property.

For instance, Obligo doesn’t make the most of a claims course of like a surety bond. As a substitute, it leverages bank-issued traces of credit score for every renter after which initiates a draw towards the road of credit score within the occasion of damages or unpaid hire. An ACH switch is distributed to the property supervisor to cowl the damages and the tenant’s fee technique on file is charged to settle the prices of the draw.

Professionals

- Enhanced renter expertise: Third-party providers provides renters better flexibility and (within the case of Obligo) may even scale back the overall prices renters should pay whereas nonetheless giving property managers the identical stage of safety.

- Automated processes: Third-party platforms typically automate their processes, decreasing the period of time spent coping with deposits for each property managers and their tenants.

- Fast entry to funds: These platforms typically supply quick entry to funds with out having to undergo a prolonged claims course of.

- Much less legal responsibility: Because you’re not liable for dealing with the safety deposit if you work with a third-party supplier, you’ll face much less legal responsibility total.

Cons

- Restricted service space: Not each third-party supplier is out there in all states. Make sure you test with any suppliers you’re contemplating to make it possible for they supply service in your space and adjust to native and state rules.

- Tenant hesitancy: Most platforms require the tenant to enroll with them and should impose further necessities, comparable to authorization for an automated withdrawal. Some residents could also be hesitant to conform. This makes it necessary to make the worth of those choices clear when selling them to renters. Drawing from the third-party service’s personal advertising materials is a simple approach to do that.

- Added charges: Use of a third-party platform generally comes at a value. Do your due diligence to verify any supplier you select matches comfortably inside your finances. Take into account offsetting any prices by providing this selection as an add-on service with a payment connected for patrons or tenants.

When to make use of third-party providers

Since most third-party platforms are digital, they are going to seemingly work greatest if the vast majority of your residents are youthful and pretty tech-savvy. They’re additionally a great match for property managers seeking to scale back handbook admin work.

3. Safety Deposit Insurance coverage

Safety deposit insurance coverage works like every other insurance coverage coverage—with one large exception: tenants are anticipated to take out a coverage with a safety deposit insurance coverage supplier and pay a month-to-month premium to maintain their coverage energetic.

The largest distinction is that the coverage isn’t meant to guard the tenant because the policyholder. As a substitute, it’s meant to guard the owner and the property supervisor within the occasion that the tenant doesn’t fulfill their obligations beneath the lease. The property supervisor is the one who has the proper to file claims, and the tenant is liable for paying again the insurance coverage firm if they should provoke a payout.

Professionals

- Insurance policies might cowl unpaid hire: In some states, property managers aren’t allowed to take unpaid hire out of a safety deposit. Nonetheless, unpaid hire could also be coated beneath a safety deposit insurance coverage coverage.

- Claims will be filed earlier than transfer out: With a standard safety deposit, property managers can’t deduct losses till the tenant strikes out of the property. However safety deposit insurance coverage suppliers help you file a declare at any level within the lease time period.

- Supplier makes selections: The coverage supplier is the one who makes the ultimate choice on any disputes, resulting in much less potential for rigidity between the tenant and the property supervisor or landlord.

Cons

- Claims will be rejected: There’s a threat that the insurance coverage firm will reject your declare, leaving you or your landlord liable for paying to repair any damages.

- Prolonged claims course of: Relying on the corporate and the complexity of the claims course of, it may take some time to obtain the funds from a payout.

- Reluctance to report points: Residents could also be reluctant to report points with the property so as to keep away from having to reimburse the insurance coverage firm for a declare.

When to make use of safety deposit insurance coverage

Safety deposit insurance coverage is usually a wise possibility should you are likely to have shorter-term tenancies. The price of carrying the sort of insurance coverage coverage can add up over time, making it much less enticing to long-term renters.

4. Lease Assure Packages

Just like a person co-signer, a lease assure program is a third-party service that agrees to take full duty for a tenant’s obligations within the occasion that the tenant defaults on their lease. The tenant pays to keep up a coverage with the lease assure program. In the event that they default, the guarantor program pays hire to the property administration firm till the lease expires or the property is re-rented and expenses the tenant for reimbursement.

Professionals

- Elevated hire safety: Lease assure applications help you proceed to gather hire even when the tenant stops paying.

- Vacancies don’t have an effect on income: Since rental earnings continues to be coming in, a emptiness gained’t have an effect on your backside line.

- Peace of thoughts: This assure offers an added stage of safety, particularly for residents who might battle to fulfill your {qualifications} on their very own.

Cons

- Residents should be accredited: With a view to use a lease assure program, residents should meet this system’s eligibility standards. Not each tenant will qualify.

- Insurance policies will be expensive: Due to the improved stage of safety supplied by lease assure applications, they will typically be costly for the tenant.

- Prolonged claims course of: Relying on this system, it will possibly take a very long time to obtain any rental earnings that you just’re owed.

When to make use of lease assure applications

Lease assure applications are widespread in high-cost areas, the place even residents with robust monetary profiles might battle to fulfill a property’s earnings or credit score necessities. They’re particularly helpful if you wish to preserve requirements excessive with out limiting your pool of certified candidates.

5. Pay-Per-Harm Packages

Pay-per-damage applications don’t cost the tenant something upfront. As a substitute, the tenant is barely charged if any damages happen throughout their keep. In the event that they do, a third-party supplier manages a secured account that lets the owner invoice the tenant for the price of damages (as much as a pre-determined restrict).

Professionals

- Wider pool of candidates: Since pay-per-damage applications include no upfront prices, you must have the ability to entry a a lot bigger pool of candidates than should you have been gathering a standard safety deposit.

- Potential for greater use charges: These applications typically boast options that make it enticing for residents to buy-in, together with the restrict on how a lot you possibly can cost for damages and the power to pay for any restore payments in installments.

- Incentive to care for the property: Because the tenant gained’t be charged something in any respect in the event that they preserve the property in pristine situation, they’ve extra incentive to abide by the lease phrases.

Cons

- Restrict how a lot you possibly can cost: Assessing the price of damages is usually subjective and these applications typically place limits round how a lot you possibly can invoice a tenant for if damages do happen.

- Elevated threat: Every program has its personal dispute decision procedures. There’s an opportunity that your harm declare could possibly be denied and your organization could possibly be pressured to shoulder the price of repairs.

- Might impose transaction charges: Since no premium is collected upfront, pay-per-damage corporations typically impose transaction charges every time you make a declare.

When to make use of pay-per-damage applications

Pay-per-damage applications are most frequently utilized in short-term rental settings, comparable to Airbnb or Vrbo, the place gathering a standard safety deposit isn’t sensible. They’re a great match when company keep briefly and turnover is excessive.

Software program to Assist Roll Out Safety Deposit Options

Providing safety deposit alternate options may help property managers fill models sooner and simplify day-to-day operations. By making leases extra accessible to a wider vary of candidates, these applications can scale back emptiness charges and ease the executive workload that comes with conventional deposits.

The suitable property administration software program could make rolling out these alternate options even simpler. Platforms comparable to Buildium convey flexibility and comfort to the whole leasing course of, for each property managers and tenants.

If you happen to’re able to see how Buildium may help you stage up your leasing, get began with a 14-day free trial (no bank card required) or schedule a personalised demo at the moment.

Learn extra on Leasing

[ad_2]