The Chase Sapphire Most popular® Card (see charges and costs) is likely one of the finest journey playing cards available on the market. With a reasonable $95 annual payment, it is a best choice for each frequent and informal vacationers — particularly these new to incomes journey rewards.

Chase is providing a powerful welcome bonus of 75,000 factors after spending $5,000 on purchases within the first three months from account opening.

In the event you’re contemplating filling out an utility, you is likely to be questioning: What credit score rating do you should be authorized for the Sapphire Most popular? Whereas there is not any set quantity that ensures approval, understanding the cardboard’s necessities may help you gauge your probabilities.

At TPG, we dedicate a whole lot of time to discussing how credit score scores work, how credit score scores affect bank card approvals and what components issuers take into account past your rating.

Let’s look at the Sapphire Most popular credit score rating necessities and the best way to enhance your probabilities of getting authorized.

Sapphire Most popular overview

The Sapphire Most popular is a longtime favourite amongst superior factors and miles collectors and inexperienced persons alike. In the event you’re contemplating including it to your pockets, now is a good time to take action.

The Sapphire Most popular earns worthwhile Chase Final Rewards factors that may be transferred to this system’s resort and airline companions. It additionally contains perks like an annual $50 resort credit score for reservations made by means of Chase Journey℠ and a ten% factors bonus in your cardmember anniversary.

To study extra, learn our full evaluation of the Sapphire Most popular.

Credit score rating wanted for the Sapphire Most popular

Credit score scores within the mid-700s and above will usually be sufficient to get you authorized for many journey bank cards. Nevertheless, having a decrease rating would not essentially imply you may’t add one among these playing cards to your pockets.

Reward your inbox with the TPG Day by day publication

Be part of over 700,000 readers for breaking information, in-depth guides and unique offers from TPG’s specialists

The Sapphire Most popular is called top-of-the-line starter journey bank cards available on the market, and inexperienced persons can nonetheless be authorized for it.

When you doubtless will not want an distinctive credit score rating to be authorized, we suggest that you’ve got a credit score rating of not less than 700 to extend your probabilities of approval. This rating falls in the midst of the “good” credit score rating class, which ranges from 670 to 739.

The credit score rating ranges utilizing the FICO scoring mannequin are:

- Distinctive: 800 to 850

- Excellent: 740 to 799

- Good: 670 to 739

- Truthful: 580 to 669

- Poor: 579 and under

Simply observe that though your credit score rating is an effective indicator of your approval odds, it isn’t an absolute science. Chase would possibly nonetheless deny you even when you meet the “required” credit score rating — and it would nonetheless approve you even when you’re under it.

The Sapphire Most popular is taken into account an excellent newbie card, however you won’t get authorized when you’ve got little credit score historical past or just one bank card to your title. If you’re brand-new to bank cards, we suggest first making use of for top-of-the-line first bank cards or a starter card to assist construct your credit score.

Many different components, equivalent to your earnings and the common age of your credit score accounts, go into qualification past your credit score rating. Chase doesn’t publicly disclose earnings or credit score utilization necessities, however a better earnings and decrease credit score utilization will enhance your probabilities of being authorized.

One other important issue that is typically ignored is your relationship with the financial institution. In the event you’ve been a longtime Chase buyer and have massive balances in your financial institution accounts with Chase, you could have higher approval odds (particularly when you apply in a department).

Lastly, even when you’re eyeing a extra premium Chase card, such because the Chase Sapphire Reserve® (see charges and costs), you could need to apply for the Sapphire Most popular first. In any case, getting authorized for the Sapphire Most popular is mostly simpler than the Sapphire Reserve.

Then, when you’re able to graduate to a extra premium product or if you’d like entry to the perks on the Sapphire Reserve at a later date, you may request a card improve.

Associated: Chase Sapphire Most popular vs. Sapphire Reserve: With new modifications in impact, which card is finest for you?

Easy methods to test your credit score rating

In no way do you have to pay to test your credit score rating. Many bank cards include a free FICO rating calculator. And even when yours would not, there are various different methods to test your credit score rating totally free.

Many free websites may help you retain higher observe of your rating and its components. You possibly can even use these companies to dispute any info in your rating that is not correct or seems to be fraudulent. If you’d like much more credit score companies, you may additionally take into account paying for a credit score monitoring service like myFICO.

Elements that have an effect on your credit score rating

Earlier than you begin making use of for any bank cards, it is important to know the components that make up your credit score rating. In any case, the mere act of making use of for a brand new line of credit score will change your rating.

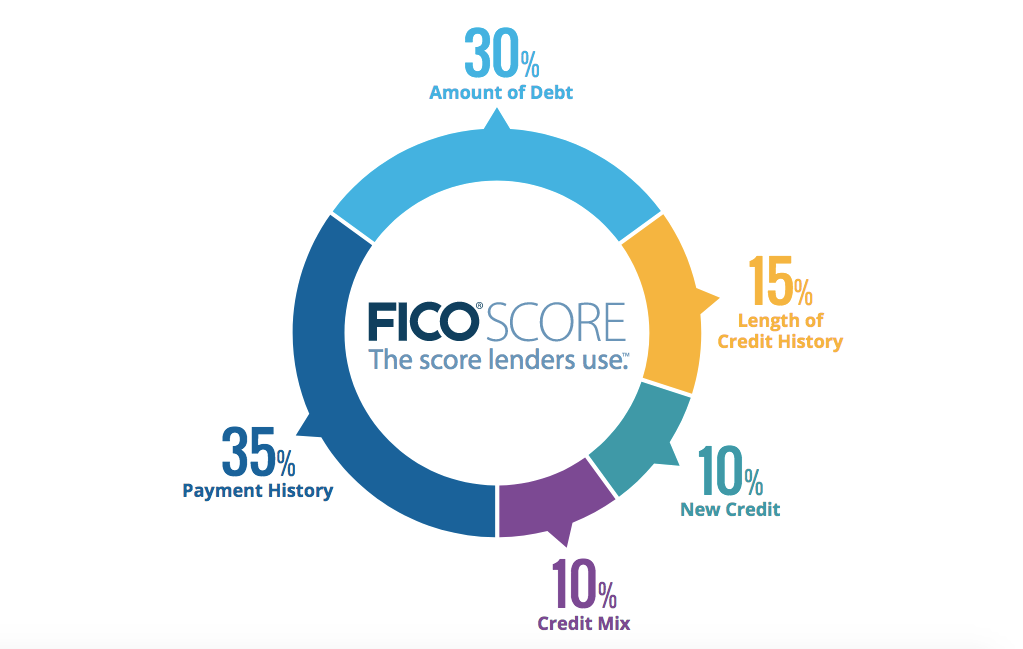

Whereas the precise method for calculating your credit score rating is not public, FICO is clear in regards to the components they assess and the weightings they use:

- Fee historical past: 35% of a FICO rating represents your fee historical past. So, when you get behind in making mortgage funds, this a part of your credit score rating will endure. Additionally, the extra prolonged and more moderen the delinquency, the extra important the destructive impact.

- Quantities owed (credit score utilization): 30% of your FICO rating consists of the relative dimension of your present debt. Specifically, your debt-to-credit ratio is the full of your money owed divided by the full quantity of credit score out there throughout all of your accounts. Many individuals declare that having a debt-to-credit ratio under 20% is finest, however it’s not a magic quantity.

- Size of credit score historical past: 15% of your rating represents the common size of all accounts in your credit score historical past. The typical size of your accounts is usually a important issue when you’ve got a restricted credit score historical past. It may also be an element for individuals who open and shut accounts rapidly.

- New credit score: Your most up-to-date accounts decide 10% of your credit score rating. So, this a part of your credit score rating will endure when you’ve lately opened too many accounts. In any case, acquiring a whole lot of new credit score is one signal of monetary misery.

- Credit score combine: 10% of your rating is said to what number of completely different credit score accounts you’ve, equivalent to mortgages, automobile loans, credit score loans and retailer bank cards. Whereas having a mixture of mortgage sorts is best than having only one kind, we do not suggest taking out pointless loans solely to spice up your credit score rating.

With regard to the Sapphire Most popular, one essential issue to contemplate is your common age of accounts. Whereas a lengthier credit score historical past will enhance your rating, many issuers concentrate on the one-year cutoff. That signifies that having a mean age of accounts of greater than a 12 months can go a good distance towards growing your odds of approval. Nevertheless, you might need bother getting authorized with 11 months of credit score historical past — even when your numerical credit score rating is great.

You probably have any delinquencies or bankruptcies in your credit score report, Chase would possibly hesitate to approve you for a brand new line of credit score. It is vital to keep in mind that your credit score profile is greater than only a quantity. Certainly, your credit score profile is a group of knowledge given to the issuer to research your creditworthiness.

Because of this, there is no such thing as a hard-and-fast rule a couple of particular credit score rating that can routinely get you authorized (or denied) for the Sapphire Most popular.

Associated: 7 issues to know about credit score earlier than making use of for a brand new card

Chase Sapphire Most popular utility necessities

After you’ve got checked your credit score rating, there’s one other Chase-related issue to contemplate earlier than you apply for the Chase Sapphire Most popular.

5/24 Rule

As with most Chase playing cards, the Sapphire Most popular is topic to Chase’s 5/24 rule, which states that Chase will routinely reject your utility when you’ve opened 5 or extra private bank cards (with any issuer) within the final 24 months.

The 5/24 rule is hard-coded into Chase’s system, so brokers typically cannot manually override it. As such, when you’re over 5/24, your solely choice for getting the Chase Sapphire Most popular is to attend till you are below 5/24 once more.

Associated: Need to open a brand new Chase card? This is the best way to calculate your 5/24 standing

What to do in case your utility is rejected

If Chase rejects your bank card utility, do not hand over. In the event you obtain a rejection letter, it’s best to first look at the explanations on your rejection. By regulation, card issuers should ship you a written or digital communication explaining what components prevented you from being authorized.

As soon as you’ve got discovered why Chase rejected you, you may name the reconsideration line.

Inform the individual on the telephone that you simply lately utilized for a Chase bank card, have been shocked to see that Chase rejected your utility and want to converse to somebody about getting that call reconsidered.

From there, it is as much as you to construct a case and persuade the agent why Chase ought to approve you for the cardboard.

For instance, if Chase rejected you for having a brief credit score historical past, you may level to your stellar document of on-time funds. Or, if Chase rejected you for missed funds, you might clarify that these have been a very long time in the past and your latest historical past has been good.

Chase can be recognized to restrict a buyer’s whole credit score line throughout all playing cards. You will have success overcoming a rejection by providing to shift unused credit score from an present card to a brand new one.

There is no assure that your name will work, however it’s price spending quarter-hour on the telephone if it would provide help to get the cardboard you need.

Associated: Your information to calling a bank card reconsideration line

Backside line

The Sapphire Most popular is a good choice for these simply getting began on the earth of factors and miles, particularly with the present welcome bonus.

Hopefully, you will not have bother getting authorized, however take into account that Chase will doubtless routinely reject you when you’ve opened 5 or extra playing cards throughout all issuers within the final 24 months.

Apply right here: Chase Sapphire Most popular Card